💥 Why Maryland’s Tax Lien System Is One Of The Most Aggressive In America

If you’re diving into the world of tax lien investing and you’ve landed on the phrase tax liens maryland, you’re already circling one of the most aggressive and controversial systems in the country. Maryland isn’t just a lien state. It’s a lien state on steroids—with a history of rapid foreclosure timelines, high interest rates, and court-backed enforcement that can either build empires or break naive investors.

Unlike many states that have layered protections for property owners, Maryland historically leaned toward the investor. Its system has attracted institutional players, hedge funds, and thousands of out-of-state investors looking for secure, government-backed returns. And the model works—if you know the risks.

But if you don’t? You’ll find yourself entangled in a legal system that moves faster than you’re ready for and cuts deeper than you expected. Because here, a tax lien isn’t just a passive instrument. It’s a weapon. And whether it helps you or hurts you depends entirely on what you understand before you buy.

💳 Chasing Tax Deeds While Drowning In Debt?

You’re not alone. Tax lien investors often have massive credit card bills, old tax debt, or business loans stacking interest while chasing properties. But here’s the good news: You may qualify for legal debt relief that wipes it out.

CuraDebt’s expert team negotiates real settlements — sometimes pennies on the dollar — while you focus on flipping deeds and building assets.

👉 See If You Qualify in 30 Seconds (Free & Confidential)

🧨 Don’t let IRS debt or credit collectors sabotage your real estate game.

🧠 Understanding The Core Mechanics Of Maryland Liens

Maryland is a classic tax lien certificate state. That means when property taxes go unpaid, the county or municipality doesn’t seize the property. Instead, it sells a lien certificate at public auction to the highest bidder. This certificate grants the investor the right to collect the unpaid taxes, plus interest and penalties, from the property owner.

The auctions happen once a year in each county. In many cases, the winning bid includes a premium over the actual tax amount owed. That premium is not refundable—it’s your risk capital. If the property redeems, you’ll receive back the tax amount and all statutory interest and fees. But you do not get the premium back. It’s the price of admission.

And here’s where Maryland separates itself. While many states offer long redemption periods—ranging from one to three years—Maryland’s redemption window can be as short as six months. After that, you can initiate foreclosure proceedings to take full ownership of the property.

So when someone asks about tax liens maryland, what they’re really asking is how fast can you foreclose, how much can you make, and what legal muscle do you need to do it?

The answer? It’s fast. It’s lucrative. And it’s not for amateurs.

⏱️ Redemption Timeline And Foreclosure Power

In most Maryland counties, the property owner has six months from the date of tax sale to redeem the property. During that period, they can repay the taxes owed, plus interest and penalties. After six months, the investor can file a complaint to foreclose the owner’s right of redemption.

This is where things escalate quickly. Once the complaint is filed, the clock starts ticking on the judicial process. If the owner fails to respond or contest the foreclosure, the court can issue a judgment transferring full title to the investor. This process, from tax sale to deed, can happen in less than a year—an unheard-of pace compared to most other states.

And that’s why investors flock to Maryland. You’re not waiting three years. You’re not earning 5% interest while holding a speculative certificate. You’re either collecting meaningful returns quickly or converting that lien into property you can flip, rent, or hold.

But this isn’t a casual system. The paperwork, court filings, and due diligence requirements are extensive. If you don’t follow the exact procedures, you’ll lose everything—including your premium. That’s what separates successful investors from those who just dabble and get burned.

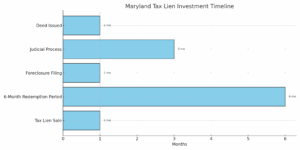

📈 Graph: Maryland Tax Sale Investor Timeline

Maryland Tax Lien Investment Timeline

The graph outlines Maryland’s hyper-accelerated lien cycle—from tax sale to court-ordered ownership in as little as twelve months. This speed is what makes tax liens maryland so appealing—and so dangerous if mishandled. Continuing the full article now.

🧨 What Happens If You Miss A Step

Most of the horror stories you’ll hear around tax liens maryland come from investors who failed to follow the rules. The process might seem simple: buy the lien, wait six months, foreclose. But that middle section—the “wait”—isn’t passive. You’re required to send notices, file motions, comply with county statutes, and prepare a legal complaint that holds up in court. Missing any part of that process doesn’t just slow you down. It invalidates your claim.

The court doesn’t care if you bought the lien fairly. If your notice wasn’t served properly, or your affidavit was filed late, or you failed to list all interested parties, the foreclosure won’t be granted. And once that window closes, your certificate could expire entirely—leaving you with a worthless document and no refund on your premium.

That’s why the most successful investors in Maryland either hire experienced attorneys or learn the legal process inside and out. Because here, the lien is just the beginning. The real work happens after you win the bid.

🧠 Understanding Premium Bidding And Overpayment Risk

Unlike Florida or Arizona, where the bid is often based on who accepts the lowest interest rate, Maryland uses premium bidding. That means you’re bidding dollars—not interest. And the highest bidder wins. But here’s the catch: the premium you pay over the base tax amount is not recoverable.

If the lien redeems, you’ll earn interest on the taxes you advanced—but not on the premium. That’s your sunk cost. If you bid too high and the owner redeems early, you may lose money even while getting paid back.

Smart investors research not just the property value, but also historical redemption rates in the county, the pace of foreclosures, and the likelihood of owner response. It’s not gambling—but it’s not guaranteed either. And without that analysis, you’re just throwing money into a system you don’t control.

This is especially critical in counties like Prince George’s and Baltimore City, where tax sales have historically included high volumes of low-value properties. Without proper vetting, you could end up holding a lien on a property that’s functionally worthless or unsellable—even if you foreclose successfully.

🏚️ The Property Itself Is Just The Start

Winning a tax lien in Maryland doesn’t give you the property. It gives you a claim. And just because the math looks good on paper doesn’t mean the real-world result will match. Many properties come with structural issues, back code violations, environmental concerns, or title complications that weren’t disclosed upfront.

You might spend $5,000 to buy a lien, then spend another $3,000 foreclosing, only to discover the property is gutted, vandalized, or part of a zoning dispute. And unless you’ve done your homework, those risks won’t show up until it’s too late.

That’s why investors who understand tax liens maryland focus not just on the auction, but on what happens afterward. They search court records. They pull environmental maps. They check for lawsuits or bankruptcy filings. And most importantly, they have an exit strategy before they ever place a bid.

📉 When The System Turns Against You

In recent years, Maryland’s tax sale process has come under scrutiny for disproportionately affecting vulnerable homeowners—especially the elderly, low-income families, and people of color. In some counties, homes were lost over tax debts as small as $250. Entire properties worth hundreds of thousands were taken and sold over what amounted to clerical issues or delayed payments.

This has led to reforms in some areas, but it’s also changed the investor landscape. There’s more media attention. More advocacy. More legal pushback. That means you, the investor, need to be even more thorough. If you move too aggressively on a redemption foreclosure, you could be sued. If you ignore legal aid groups or media inquiries, you could end up in the news. And not in a good way.

Understanding tax liens maryland today means understanding that the rules are shifting. You need to be both profitable and ethical—or risk blowback that can tank your entire business.

🔎 Final Word On Maryland Lien Strategy

Maryland offers one of the fastest, most lucrative tax lien systems in the country—but only for those who respect its complexity. You can make double-digit returns. You can own properties at steep discounts. But you can also lose everything you bid, end up in court, or spend years trying to clear a messy title.

The system favors those who prepare. Who learn. Who respect the law. The county will not hold your hand. The courts will not give you a second chance. And the property owner may not redeem—so your decision to foreclose better be backed by strategy, not emotion.

If you’re ready to play this game at a high level, Maryland might just be the fastest way to grow a tax lien portfolio with real cash flow and equity. But if you’re not ready? Stay far away. Because this state will eat you alive.

👉 Trying to make sense of that notice you got in the mail? Has the IRS Sent You a Notice?