When a Quiet State Plays the Loudest Game With Your Equity

Massachusetts may not be the first state people mention when they talk about tax sales, but that’s exactly what makes it dangerous. It doesn’t need hype. It doesn’t need headlines. It just needs statute, silence, and time. The Massachusetts tax lien sale system is built on one thing: quiet legal authority. And if you’re dealing with Massachusetts redemption deeds, you need to understand one brutal fact—the rules here are old, sharp, and unapologetically in favor of the municipality.

This isn’t a tax lien state. This isn’t a deed state. Massachusetts operates in its own lane. And that lane leads straight to court. The tax sale process in this state is quiet on the surface but packed with traps under every step. It starts with unpaid taxes—but it ends with judges, auctions, foreclosures, and lost homes. You can’t play this game casually. You either learn how it works, or you lose your footing and the property all in one swing.

Municipalities Foreclose Through the Courts—Not the Market

In most states, counties sell tax liens or deeds directly to investors. But in Massachusetts, when a taxpayer fails to pay, the city or town itself initiates foreclosure proceedings in Land Court. That’s right—they sue for ownership. They don’t sell you paper. They don’t auction off the debt. They go straight for the jugular.

This is where most people get blindsided. Because the town becomes the petitioner. They’re not neutral. They’re the ones trying to take the property, and they use the full force of the court to do it. You don’t get a grace period. You don’t get a hearing unless you file one. You get a docket number and a deadline. And once that deadline passes? Your redemption rights start to vanish.

Once judgment enters, the town becomes the legal owner. No redemption. No repayment plan. It’s over. Forever.

Investors Only Get In When the Town Sells the Deed

If you’re thinking this is your next investment play, understand how late to the game you really are. In Massachusetts, investors don’t buy liens. They buy tax title properties that the town has already foreclosed on. These deeds are offered by the town after they’ve gone through court, cleared title, and taken ownership.

You’re not buying paper. You’re buying property the town doesn’t want. And you’re buying it on their terms. They choose when to sell. They choose what to offer. And they usually set the sale price far above the taxes owed. Why? Because they’ve paid the legal fees. They’ve handled the title. And now, they want equity—not just reimbursement.

So if you’re chasing Massachusetts tax lien sale inventory, you’re not going to a public auction. You’re going to town hall, asking who’s on the list, and hoping they let you in the door.

Redemption Can Be Shut Down Without Warning

The scariest part of this process is how fast redemption ends. You may receive notice that your taxes are delinquent. Then a court date. Then a judgment. Then—nothing. It all happens without high drama. No screaming. No auctioneer. Just a judge quietly recording a judgment that says your property no longer belongs to you.

If you’re not watching the mail. If you’re not opening certified letters. If you’re out of state or the address on file is wrong? You’ll miss it. And once the redemption period expires under the judgment, it cannot be reversed.

No grace. No reinstatement. Just permanent loss.

This is how the towns have taken back hundreds of properties across Massachusetts in the past five years. Quietly. Legally. Without fanfare.

Title Isn’t as Clean as You Think

Even after foreclosure, municipalities often struggle to sell tax title properties because the title is viewed as toxic by many lenders and buyers. Massachusetts uses a Torrens system (Land Court recording) for some properties, but many still fall under registry systems that don’t automatically wipe junior liens or claims.

What does that mean? It means even after the town forecloses and you buy the property, title insurance may still be denied. Buyers may still walk. Quiet title actions may still be needed. And until then, you’re holding something the bank sees as a lawsuit risk, not an asset.

This becomes especially true if federal tax liens, environmental liens, or missing heirs exist. Even the Land Court judgment doesn’t always clear them. And that’s your problem now.

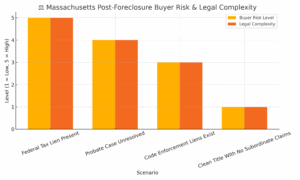

Here’s what typically happens after judgment:

| Post-Foreclosure Scenario | Likely Buyer Risk | Legal Remedy Required |

|---|---|---|

| Federal Tax Lien Present | Very High | IRS Release/Discharge |

| Probate Case Unresolved | High | Quiet Title |

| Code Enforcement Liens Exist | Moderate | Settlement/Abatement |

| Clean Title With No Subordinate Claims | Low | Immediate Transfer OK |

So if you plan to flip or develop, expect delays. Expect to hire attorneys. And expect towns to disclose very little up front.

The Town Holds All the Power

Unlike in other states where investors dictate pricing and demand, in Massachusetts, it’s the town that holds the cards. They determine which properties go up for sale. They decide whether to use auctions, sealed bids, or private transfers. They can bundle properties, restrict buyer qualifications, and cancel sales without notice.

You don’t control the terms. They do.

And once you buy? Don’t expect help. If a neighbor claims an easement, if an underground oil tank leaks, if the roof collapses—you’re on your own. The town washed its hands the moment you paid.

This isn’t a partnership. It’s a handoff.

💳 Chasing Tax Deeds While Drowning In Debt?

You’re not alone. Many investors rack up credit cards, business loans, or even owe the IRS — all while trying to flip tax deeds or build passive income with liens. The result? Debt piles up while returns take years.

But here’s the fix: CuraDebt can help settle your debts legally — sometimes for pennies on the dollar. It’s fast, confidential, and designed for real estate investors who need breathing room.

👉 See If You Qualify In 30 Seconds (Free & Confidential)

🧨 Don’t let IRS debt or credit cards sabotage your tax lien strategy.

Redeemed Properties Still Leave Scars

For homeowners who do redeem before final judgment, the cost is brutal. Massachusetts law allows municipalities to tack on 18% interest, legal fees, and court costs. That means a $4,000 delinquency can become a $12,000 bill with zero flexibility.

Even after redemption, the record of foreclosure proceedings remains. That means lenders, insurers, and title companies may flag the property as high risk—even if ownership never changed. You beat the foreclosure. But the scars are permanent.

If you’re a homeowner in Massachusetts behind on taxes and you think you can “wait it out,” you’re wrong. This system doesn’t drag its feet. It quietly enforces its will. And once the judgment enters, the path back to ownership is closed forever.

If you’ve received a notice—or even think one might be coming—you need to act immediately.

Use this link to get help understanding the notice:

https://www.executivetaxsolution.com/irs-decoder.html

The window to fix this shuts fast. And once it does, the court won’t reopen it—no matter how loud you scream.